When it comes to charity investment portfolios, putting in place the right strategy and finding the correct balance between risk and return, isn’t as easy as it may seem. Here are some of the risks trustees should be aware of and how you can get the balance right.

The impact of unbalanced risk and return – an example

Whether endowments or long-term assets, a common reason for charities investing is to provide income while preserving the real value of their investments. If achieved, this can allow the charity to help fund its ongoing activities and deliver its objects indefinitely. The following example considers a charity with this investment objective. It highlights how if the balance between the income sought, the investment risk taken and the investment amount is not correct at outset; the ability of the charity to fulfil this objective can quickly diminish.

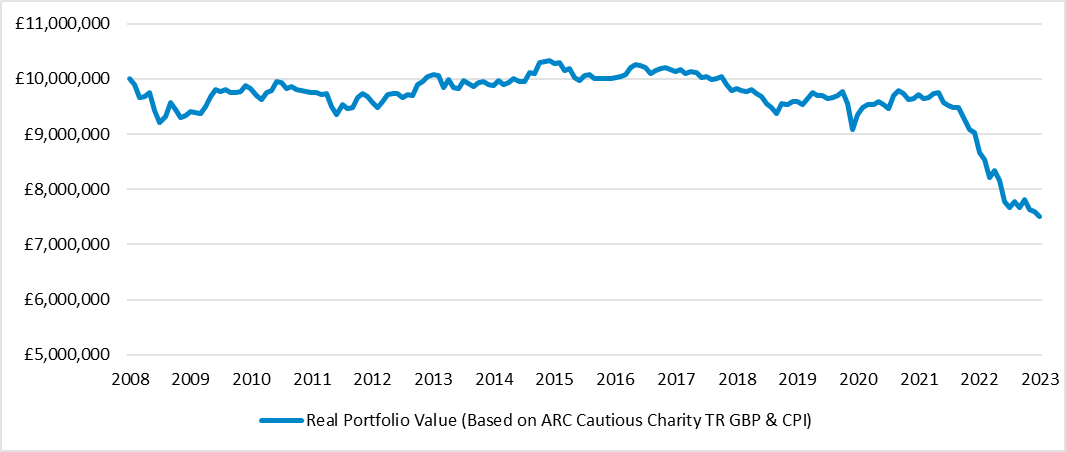

This chart considers a charity whose trustees decided to invest £10million 15 years ago and take an income from the investments of £150,000 per annum (1.5% of the original investment), increasing in line with inflation. It assumes the charity has invested at a ‘Cautious’ risk level and shows the portfolio value over time in real terms.

Notes: At a ‘Cautious’ risk level we would typically expect to see exposure to equity-type risk assets of around 40%. This chart is based on data for the ARC Charity Cautious Index. 35 investment firms currently contribute data to the Asset Risk Consultants (ARC) Charity indices, providing a good indication of the average performance of UK Charity discretionary managers for this risk level after charges. Figures are adjusted for inflation (as measured by CPI) to show the purchasing power of assets over time. This data has been obtained from Morningstar Advisor Workstation. Past performance is not a reliable indicator of future return. Investment values and any derived income can fall as well as rise.

Over the 15 years to 2023, a charity which invested in this way would have seen their £10million portfolio fall in real value to be worth approximately £7.5million in today’s terms. In addition to the reduced capital, the annual income, having increased with inflation, would now represent over 3% p.a. of the portfolio value. This would put the charity in a position where to continue to meet its objectives, it would have to significantly reduce its income requirement, increase risk, or a combination of the two. Even at a ‘Balanced’ risk level over the full period, this charity’s portfolio would be worth less in 2023 than at the point of initial investment.

We help charities mitigate these risks by thoroughly examining their circumstances, attitude to risk, capacity for loss, level of ‘risk need’ and ensuring that their strategy aligns with these and is independently reviewed on a regular basis, to ensure it remains on track.

Getting the balance right

Setting investment objectives and strategy

The starting point for developing an investment strategy is setting objectives and these are unique to each charity. By clearly articulating them, you can establish a framework that guides your charity’s investment decisions and ensures alignment between your investments, charitable purpose and trustees’ duty to maximise financial returns within an acceptable level of risk.

Objectives should clearly identify what your charity is seeking to achieve in investing its assets and over what timescale. As they will be individual to your own charity and its objects, it’s challenging to provide guidelines that a wide range of charities can follow. The same can be said about determining what proportion of assets your charity should invest – what assets are needed for the short term? What does your charity’s cashflow look like? Do you need your investments to generate income?

Setting objectives and developing an investment strategy involves the consideration of your charity’s short-term and long-term financial commitments, expected income, the possibility of unforeseen needs and, where applicable, any limitations on restricted funds. Having a thorough understanding of investments to ensure objectives remain realistic, relevant and achievable is also important, and is why many charities take professional advice around strategy and setting appropriate objectives for their investments as part of that.

Finding the right approach to risk

Adopting a suitable approach to risk is a process that we often see trustees contend with. There’s good reason for this – it’s something which individual trustees or beneficiaries of your charity are likely to have differing opinions on. It’s also an area that, if not undertaken in the right way, can have serious consequences for a charity. Understanding the various risks that can impact your charity’s investment portfolio and managing these effectively is crucial for ensuring the long-term ability of your investment solution to meet your objectives.

There are many different forms of risk that may apply to different types of investment. Considering a charity investment portfolio, there are four main risks that we believe trustees should have a full understanding of: volatility, inflation, income and reputational.

Volatility, or market risk, is inherent to investments. Financial markets can experience fluctuations that cause the value of investments to rise or fall unexpectedly. When it comes to investing, the risk warning that is, rightly, displayed everywhere, is one that states that you may get back less than you originally invested. This risk is heightened when investing over shorter timeframes. Charities should therefore develop investment strategies that take into account time horizons and the tolerance to fluctuations in value that the organisation can accept for their invested assets. Regular monitoring can help charities stay on track and make informed decisions in response to market volatility.

Inflation erodes the purchasing power of funds over time. The recent sharp rise in inflation has brought this risk to the forefront of many investors’ minds. Over the last twenty years, inflation has averaged just less than 3% a year. The long-term return expectations of different asset classes are not the same. To ensure your charity’s investments will at least retain their purchasing power, or grow it, over the long-term, the allocation to different assets should be considered. Too much exposure to the typically higher returning asset class of equities can increase the market risk but conversely too much exposure to lower risk assets such as cash and bonds can increase inflation risk.

Income risk is another consideration if your charity is to rely on investment income to support your activities. Investments can be a great source of income for charities but fluctuations in interest or dividend payments can impact the cash flow generated from investments. Targeting income too heavily could also detract from capital growth, potentially harming the future ability of your investments to meet income needs.

Reputational risk can be significant for charities because public image and trustworthiness can play a critical role in attracting support and funding. If any of your investments conflict with your charity’s objects, this image and trust can quickly diminish. An example of this would be a charity helping people with addiction discovering underlying investments in companies involved in the tobacco or gambling industries within their portfolio, or an environmental charity discovering significant fossil fuel exposure. Trustees must be mindful of the potential reputational risks associated with certain investment decisions. Thankfully, these risks can be mitigated through thorough due diligence, well-written policies, clear dialogue with your investment manager and regular reviews of your investments.

These four risks apply to most charity investments. However, depending on the nature of your charity’s investments and cash reserves, liquidity, currency, principle, counterparty or default are all additional risks that may apply and may need careful thought.

What should you do?

When it comes to strategy, trustees don’t have an easy job. You’ve got to ensure you’re doing what’s in the best interests of the charity and its beneficiaries while managing the balance of risks.

Your charity’s investment strategy and approach to risk should not be taken lightly, nor should they be seen as one-off exercises. Reviewing them regularly and when there are changes in circumstances, such as changes to the board of trustees or changes to income and expenditure, demonstrates good governance and ensures solutions remain appropriate. As well as ensuring you have an appropriate investment strategy and approach to risk, before investing charity assets, trustees also need to have in place an Investment Policy Statement (IPS). You can read more about IPSs here.

Professional investment consultancy advisers can help you navigate the challenging balancing act of obligations, objectives, and risk, ensuring that the correct foundations are laid for your charity’s investments and performing regular reviews to make sure you stay on track.

Authored by Seth Dowley - Senior Manager at Buzzacott

Access all our articles and search the provider directory for free.

{kind=link}